A health-aware retirement product, under your brand.

Investment management is commoditising. Differentiation needs a new lever. PensionPulse is offered to independent advisors as a white-label tool that adds a personalisation layer to every client relationship — and creates regular, meaningful touchpoints between scheduled reviews.

In a controlled study of 1,151 professional financial advisors, giving them client-specific longevity information shifted their recommendations by 25–91%. PensionPulse puts that kind of signal in your hands — from passive trajectory data, not a questionnaire.

See the researchFour shifts in the advisor's economics.

Conversations get richer

A traditional review covers portfolio performance, risk allocation, and progress against the plan. With PensionPulse on the table, the conversation extends to how the client is actually aging and what that means for the realistic horizon of their plan.

Differentiation is concrete

In an industry where investment-management services are commoditising, advisors who offer a genuinely distinctive client experience defend their margins better. A health-aware retirement product is not yet a commodity.

Retention has a new mechanism

Clients who return to the application weekly are clients who do not switch advisors lightly. The engagement loop keeps your brand in the client's life between formal reviews.

No development burden

Offer a sophisticated, branded product without building software, hiring developers, or carrying ongoing maintenance. The platform's roadmap is your roadmap.

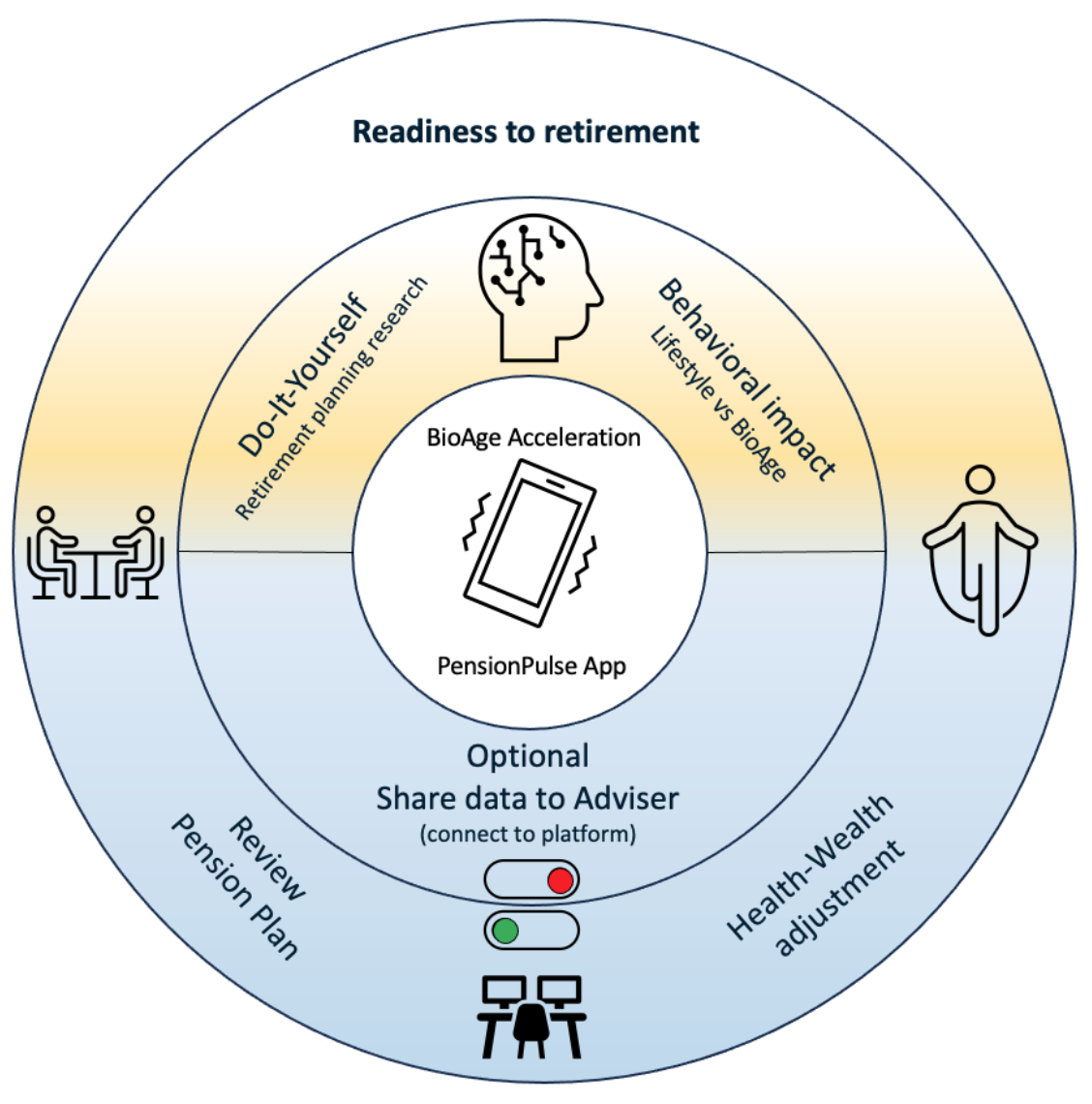

Same advisor–client structure, with a continuous information layer.

Most of the loop runs in the client's hands — research, lifestyle, day-to-day adjustment. The advisor enters at the formal review, optionally connecting to the same data when the client agrees to share.

Portfolio performance and progress against the plan stay on the agenda. Beside them: how the client is actually aging and whether the realistic horizon of the plan still matches the trajectory.

Clients open the app weekly to see their indicators. That keeps your brand present in their life and keeps their attention on health and retirement goals between the formal touchpoints you control.

The platform makes a causal chain visible in the client's head: a healthier lifestyle moves the aging-speed signal, and a slower aging speed makes the retirement plan more affordable and more enjoyable. The motivation for lifestyle choices and the motivation for financial choices stop being two separate conversations.

The hardest part of advice isn't the meeting.

It's staying present in the client's life between meetings — where the relationship is actually won or lost. A continuous signal does that quiet work for you.

Quarterly reviews become weekly touchpoints — the client opens the app, your brand is there between meetings.

A continuous reason to stay engaged, not an annual statement that arrives and is forgotten.

Conversations anchored in the client's own aging trajectory, not just portfolio performance.

Health and money stop being two separate conversations.

A familiar process, with one new column.

PensionPulse doesn't change the six phases of retirement planning your practice already runs. It adds a health-aware lens at each one — surfaced where the existing workflow already pauses for review.

The phase and role labels follow standard financial-planning practice. The BioAge column is what PensionPulse contributes — slotted into the points in the process where you'd be reviewing or revising the plan anyway.

Pick what you'd want to see in a demo.

How PensionPulse strengthens my brand

White-label: your logo, colours, and name on the splash screen, in-app header, and report footer.

Request this in a demoHow I stay present between meetings

Client Q&A threads and notifications go out under your firm — not ours.

Request this in a demoHow trajectory signals reach me

An aging-speed signal stream flags when a client's trend changes enough to warrant a review.

Request this in a demoHow regular reports look under my logo

A full retirement report, branded as yours, that you can generate on a regular cadence.

Request this in a demoBuilt to feed your stack, not replace it.

PensionPulse keeps a single source of truth for every report, with the same numbers rendered to every surface — the in-app view, a PDF for the client file, and a structured export. That architecture means a longevity assumption can flow into the leading planning platforms advisors already use — Income Lab, RightCapital, eMoney, MoneyGuide — as those integrations come online.

PensionPulse is architecturally ready for integration. Structured export and named-platform integrations are not live today.

What the tool changes in day-to-day work.

Beneath the economics and the workflow integration, three shifts happen at the human level — in what you can say to a client, and how often you can say it.

Recommendations get personal

Withdrawal rate, allocation, target retirement age — each anchored to the trajectory of the person in front of you, not a population average. The same six decisions you'd make anyway, with a personal input instead of a generic one.

Sensitive conversations get facts

Life expectancy, longevity, the realistic horizon of the plan — some of the hardest conversations in advisory work, because there is rarely client-specific data to ground them in. A measured aging trajectory lets you have them on the client's own evidence rather than averages or speculation.

Cadence of contact rises

Quarterly meetings turn into weekly touches. The client opens the app to see their indicator; your brand sits in the moment; and when the formal review comes the relationship has been continuous rather than episodic.

Not every practice model fits equally.

PensionPulse fits most naturally with practitioners whose primary deliverable is comprehensive advice rather than product transactions. In other models the integration is shallower. We say so up front because the channel matures fastest where the natural fit is highest.

- · Comprehensive advice as primary deliverable

- · Periodic in-depth plan reviews

- · Differentiation through depth rather than breadth

- · Direct, long-horizon client relationships

- · Transaction-led practice models

- · Short-cycle product distribution

- · Practices where client touchpoints are infrequent

Cover the client's premium subscription on their behalf.

Advisors can offer to pay for a client's premium subscription on the client's behalf. A tool for advisors who want to demonstrate care for premium clients, or who run engagement programmes for specific cohorts — without requiring the client to open their wallet.

Both advisor and client accept through a separate flow.

Sponsoring does not grant the advisor visibility into client data.

Advisor terminates: client gets notice and a grace period. Client terminates: ends immediately.

Workspace seat licence + sponsorship.

Straight answers, within the guardrails.

Is this a medical diagnosis or a medical device?

No. It’s a wellness signal describing aging speed, not a diagnosis. We lead with the gap to calendar age rather than an absolute number, and every report carries persistent health and non-advisory disclaimers.

Talk to us about thisDoes it give investment advice instead of me?

No. PensionPulse is a signal, not advice. It informs the conversation you have with your client; you remain the advisor. Human-in-the-loop by design.

Talk to us about thisWhat happens to my client’s data, and who consents?

Sharing is bilateral and consent-based. Until the client grants advisor consent, their report and signals are hidden from you. The client’s data stays the client’s.

Talk to us about thisDoes this fit my kind of practice?

Strongest fit: comprehensive-advice practices with periodic in-depth reviews and long-horizon client relationships. Partial fit: transaction-led, short-cycle models with infrequent touchpoints.

Talk to us about thisWhat does it cost?

The commercial model is a workspace seat licence plus optional sponsored client subscriptions. Pricing and these tiers are P2 · upcoming — contact us and we’ll discuss whether PensionPulse fits.

Talk to us about thisTalk to us about your practice.

We're onboarding advisors selectively in early markets. Reach out and we'll discuss whether PensionPulse fits.